Building wealth isn’t just about earning more money—it’s about how you think about and use the money you already have. At its core, the wealthy mindset isn’t defined by the size of your paycheck but by your approach to financial decisions. The key shift? Moving from a spending-focused mindset to an investing-focused one.

Understanding the Difference: Spending vs. Investing

Spending is transactional. You exchange money for goods or services, and once the transaction is complete, the money is gone. Investing, on the other hand, is strategic. It involves putting money into assets or opportunities with the expectation of generating future returns.

For example:

- Spending: Buying the latest smartphone or a luxury car.

- Investing: Purchasing stocks, real estate, or starting a side business.

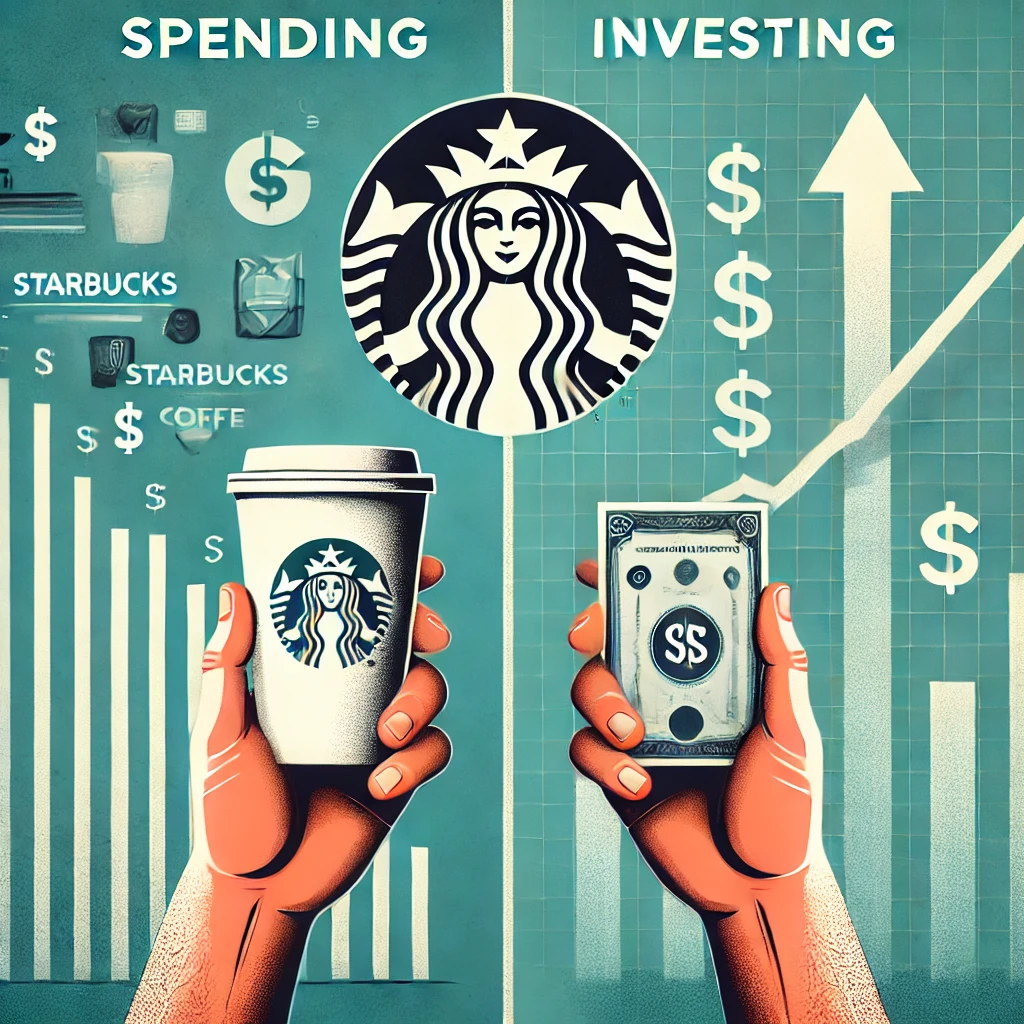

- Real-Life Example: Instead of spending $5 every day on a Starbucks coffee, you could invest that $5 into Starbucks stock. Over time, the stock could grow in value, provide dividends, and potentially yield far greater returns than the short-term pleasure of a daily coffee.

While spending satisfies immediate desires, investing builds long-term financial stability and wealth.

The Mindset Shift

To cultivate a wealthy mindset, you must view money as a tool for growth, not just consumption. Here are key principles to adopt:

- Focus on Assets, Not Liabilities: Prioritize purchases that appreciate in value or generate income.

- Delayed Gratification: Resist impulse spending and prioritize long-term financial goals.

- Continuous Learning: Stay informed about financial markets, investment opportunities, and wealth-building strategies.

- Make Your Money Work for You: Passive income streams, such as dividends or rental income, can create financial freedom.

Practical Steps to Start Investing

- Set Clear Financial Goals: Understand what you’re investing for—retirement, financial independence, or a specific milestone.

- Start Small: You don’t need large sums to begin investing. Even small, consistent contributions can grow significantly over time.

- Diversify Your Investments: Spread your money across different assets to minimize risk.

- Automate Investments: Set up automatic transfers to your investment accounts to ensure consistency.

Overcoming Common Barriers

- Fear of Risk: Educate yourself to make informed decisions and understand that all investments carry some level of risk.

- Lack of Knowledge: Use resources like FutureFinanceLab.com to expand your financial literacy.

- Instant Gratification Culture: Remind yourself of the long-term benefits of investing.

Final Thoughts

Adopting a wealthy mindset isn’t about restricting yourself from enjoying life. It’s about aligning your financial habits with your long-term goals. Every dollar spent is a choice—a choice between fleeting pleasure and future security.

At Future Finance Lab, we believe in equipping individuals with the tools and knowledge to make smarter financial choices. Shift your focus from spending to investing, and watch how your financial future transforms.